The FIRE (Financial Independence, Retire Early) movement has gained massive popularity in recent years, inspiring individuals and families to rethink their financial goals and lifestyle choices. While many FIRE advocates often focus on dual-income households or single individuals, achieving FIRE with a single income is not only possible but also rewarding. Here’s a comprehensive guide to navigating the path to financial independence for a single-income family.

1. Overview of Steps to Achieve FIRE for a Single-Income Family

A. Build a Solid Financial Plan

A robust financial plan is the cornerstone of the FIRE journey. Here are the key components:

- Set Clear Goals: Determine what financial independence and early retirement mean for your family. Establish clear, achievable milestones.

- Create a Budget: Develop a realistic budget that tracks all income and expenses. This will help identify areas where you can cut back and increase savings.

- Emergency Fund: Build an emergency fund covering 6-12 months of living expenses to safeguard against unexpected events like job loss or medical emergencies.

B. Maximize Income

While having a single income might seem limiting, there are strategies to maximize earnings:

- Career Advancement: Pursue promotions, additional certifications, or education that could lead to higher-paying roles.

- Side Hustles: Consider part-time work or side gigs that can bring in additional income without compromising family time.

C. Minimize Expenses

Cutting unnecessary expenses is crucial for increasing your savings rate. Here’s how to do it effectively:

- Living Below Your Means: Adopt a frugal lifestyle, focusing on needs rather than wants. This might mean downsizing your home, driving a more economical car, and eliminating luxury expenses.

- Debt Reduction: Prioritize paying off high-interest debt. Once debts are cleared, the money previously used for payments can be redirected towards savings and investments.

- Smart Shopping: Use coupons, buy in bulk, and prioritize sales and discounts to reduce everyday expenses.

D. Invest Wisely

Investing is essential for those pursuing FIRE, as it allows your savings to grow exponentially. Consider these strategies:

- Diversified Portfolio: Invest in a mix of stocks, bonds, real estate, and other assets to spread risk.

- Low-Cost Index Funds: These offer broad market exposure with low fees, making them an excellent choice for long-term growth.

- Retirement Accounts: Maximize contributions to tax-advantaged accounts like IRAs and 401(k)s to benefit from tax savings and compound growth.

Now, let’s dive into the details.

2. Building a Solid Financial Plan for Your FIRE Journey

The journey towards Financial Independence, Retire Early (FIRE) is deeply rooted in the formulation of a solid financial plan. This plan acts as a roadmap, guiding you through various financial milestones and ensuring you remain on track to achieve your goals. Creating a robust financial plan involves several key components, each playing a crucial role in your overall strategy. Here’s a detailed look at how to embark on this transformative journey.

Setting Clear Goals

One of the foundational steps in building a financial plan for FIRE is setting clear, specific goals. It’s not just about wanting to retire early; it’s about defining what early retirement looks like for you and your family. Consider the following steps to set effective goals:

Define Financial Independence: Clarify what financial independence means to you. Is it the ability to quit your job and travel the world, or simply having the freedom to choose work that aligns with your passions without worrying about the paycheck?

Establish Milestones: Break down your ultimate goal into smaller, achievable milestones. For instance, you might set goals to save a certain amount of money within the first five years, pay off debt within ten years, and so on.

Prioritize: Decide which financial goals are most important and focus on those first. This might include paying off high-interest debt, saving for a down payment on a house, or building a substantial investment portfolio.

Clear goals provide direction and motivation, making the long journey towards financial independence more manageable and less daunting.

Creating a Budget

A solid budget is the backbone of any financial plan. It provides a clear picture of your income and expenses, helping you make informed decisions about where to allocate your resources. Here’s how to create a budget that supports your FIRE goals:

- Track Income and Expenses: Start by keeping a detailed record of all your income sources and monthly expenses. This includes everything from your salary and side hustle earnings to rent, groceries, and entertainment.

- Identify Savings Opportunities: Analyze your spending to identify areas where you can cut back. Perhaps you’re spending too much on dining out or have subscriptions you don’t use. Redirect these savings towards your FIRE goals.

- Allocate Funds Wisely: Divide your budget into key categories: needs, wants, and savings. Needs are essential expenses like housing and utilities, wants are discretionary expenses, and savings are funds earmarked for your future. Aim to increase the proportion of your budget allocated to savings over time.

- Regular Reviews: Periodically review and adjust your budget to reflect changes in your income, expenses, and financial goals. This ensures you stay on track and can adapt to any unexpected financial changes.

A realistic, well-planned budget is essential in maximizing your savings potential and ensuring you live within your means.

3. Maximizing Your Income for the FIRE Journey

Achieving Financial Independence and Retire Early (FIRE) often requires more than just cutting expenses and saving diligently—maximizing your income is a key component of this journey. While having a single income might seem limiting, there are several effective strategies to boost your earnings and accelerate your path to financial independence. Below are some detailed approaches to maximizing your income:

Career Advancement

Climbing the career ladder can significantly increase your earnings and propel you closer to your FIRE goals. Here’s how you can leverage career growth to maximize your income:

- Pursue Promotions:

- Performance Excellence: Consistently deliver high-quality work and exceed your job expectations. This often leads to recognition and promotional opportunities.

- Networking: Build strong professional relationships within your industry. Networking can open doors to new opportunities and career advancements.

- Further Education and Certifications:

- Advanced Degrees: Consider obtaining advanced degrees relevant to your field. An MBA, for example, can open up higher-paying management roles.

- Professional Certifications: Certifications can enhance your skills and expertise, making you more marketable and eligible for raises and promotions. Examples include PMP (Project Management Professional) for project managers or CISSP (Certified Information Systems Security Professional) for cybersecurity experts.

- Skill Development:

- Continuous Learning: Stay updated with the latest trends and technologies in your industry. Participate in workshops, webinars, and online courses to continually enhance your skill set.

- Soft Skills: Develop essential soft skills such as leadership, communication, and negotiation. These are highly valued by employers and can differentiate you from your peers.

Side Hustles

Side hustles can provide a substantial boost to your income without necessarily disrupting your full-time job or family time. Here are some effective side gig ideas:

- Freelancing:

- Consulting: Offer consulting services in your area of expertise. Many companies seek experienced professionals for short-term projects.

- Creative Services: If you have skills in writing, graphic design, web development, or photography, consider offering freelance services on platforms like Upwork or Fiverr.

- Part-Time Jobs:

- Tutoring or Teaching: Use your knowledge to tutor students in subjects you excel in or teach a language, musical instrument, or other skills.

- Ridesharing or Delivery Services: Companies like Uber, Lyft, DoorDash, or Amazon Flex offer flexible hours and can be a convenient way to earn extra income.

- Online Ventures:

- Blogging or Vlogging: If you have a passion or expertise to share, consider starting a blog or YouTube channel. With effort, these platforms can generate income through advertisements, sponsorships, or affiliate marketing.

- E-Commerce: Start an online store using platforms like Etsy, Shopify, or eBay to sell handmade crafts, vintage items, or other products.

Read more on Side Hustles to Accelerate Your FIRE Journey

4. Minimizing Expenses for Your FIRE Journey

Achieving Financial Independence and Retire Early (FIRE) is not solely about increasing income; it’s equally important to manage and minimize your expenses effectively. By cutting unnecessary expenses and adopting smarter financial habits, you can significantly increase your savings rate and accelerate your path to financial freedom.

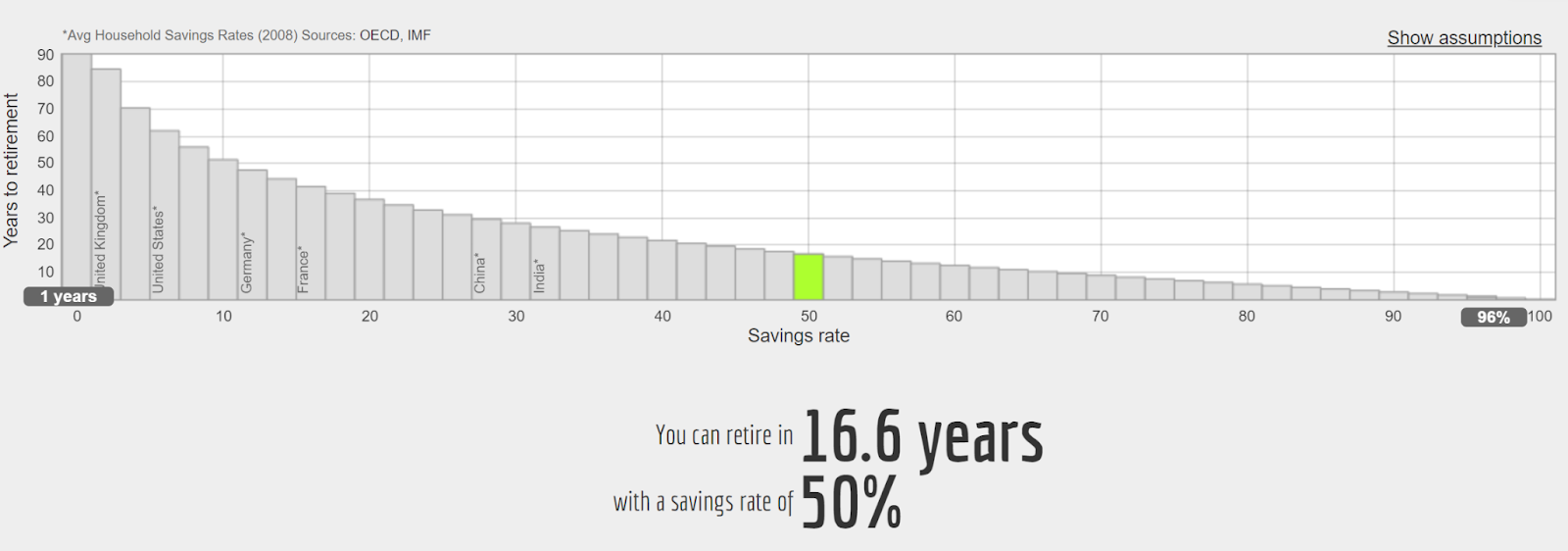

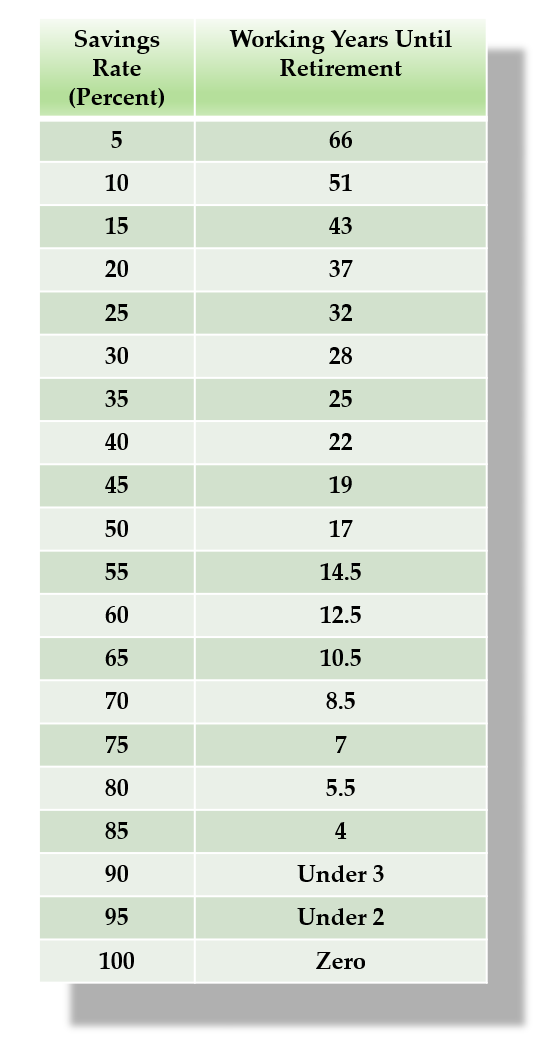

Savings rate has a direct correlation to the years to financial independence. If you save a substantial percentage of your take-home pay, such as 50%, and live on the remaining 50%, you’ll be financially independent in a reasonable number of years—about 17 years, according to networthify.com.

The table below from Mr. Money Mustache shows how many years you will have to work for a range of possible savings rates, starting from a net worth of zero:

The charts are based on some conservative assumptions, including:

- You can earn a 5% return on your investments after inflation during your saving years.

- You’ll live off the “4% safe withdrawal rate” after retirement, with some flexibility in your spending during recessions.

- You want your ‘Stash to last indefinitely, touching only the gains.

So you see, the importance of your savings rate cannot be overstated. Saving more and investing those savings wisely to achieve a reasonable return is crucial. Let’s take a closer look at how to effectively minimize your expenses first:

Living Below Your Means

Living below your means is fundamental to achieving financial independence. This involves making conscious decisions to prioritize essential needs over discretionary wants. Here’s how to embrace a more frugal lifestyle:

- Downsize Your Home:

- Evaluate Housing Needs: Assess whether your current living situation fits your needs. Often, a smaller, less expensive home can help to significantly reduce mortgage or rent payments, property taxes, and utility costs.

- Consider Relocation: Moving to an area with a lower cost of living can lead to substantial savings on housing, groceries, transportation, and other daily necessities.

- Economical Transportation:

- Drive a Fuel-Efficient or Used Car: Choose vehicles that are fuel-efficient and have low maintenance costs. Buying quality used cars instead of new ones can save money on both the purchase price and insurance premiums.

- Use Public Transportation: If your living situation permits, utilize public transportation, carpool, or bike to save on gas, parking, and maintenance.

- Eliminate Luxury Expenses:

- Cut Unnecessary Subscriptions: Review your monthly subscriptions and memberships. Cancel those you rarely or never use, such as streaming services, gym memberships, or magazines. Utilize budgeting apps like WeFIRE to help you automatically review your subscriptions regularly to identify any unnecessary ones.

- Simplify Your Lifestyle: Focus on free or low-cost leisure activities. Instead of dining out, cook meals at home. Engage in outdoor activities, visit local parks, or host game nights with friends.

Debt Reduction

Excessive debt, especially high-interest debt, can be a significant barrier to achieving financial independence. Prioritizing debt reduction can free up funds for savings and investments. Here’s how to approach it:

- Assess Your Debt:

- List Debts: Compile a comprehensive list of all your debts, including credit cards, personal loans, student loans, and mortgages. Note the interest rates and minimum payments for each.

- Create a Payment Plan:

- Prioritize High-Interest Debt: Focus on paying off high-interest debt first (debt avalanche method), as it accumulates the most interest over time. Alternatively, you can use the debt snowball method, starting with the smallest debt to gain momentum.

- Consolidate Loans: If possible, consolidate multiple high-interest debts into a single, lower-interest loan. This can simplify your payment process and reduce the amount of interest paid over time.

- Avoid Accumulating New Debt:

- Limit Credit Card Use: Use credit cards responsibly, ensuring that you pay off the balance in full each month to avoid interest charges.

- Emergency Fund: Maintain an emergency fund to cover unexpected expenses, reducing the need to rely on credit.

Smart Shopping

Adopting smart shopping habits can lead to significant savings on everyday expenses without compromising your quality of life. Here are effective strategies to reduce your spending:

- Use Coupons and Discounts:

- Clip Coupons: Regularly use coupons from newspapers, online sources, or store apps for grocery shopping and other purchases.

- Buy in Bulk:

- Wholesale Clubs: Join wholesale clubs like Costco or Sam’s Club to buy non-perishable items, household supplies, and other frequently used products in bulk. This often reduces the per-unit cost and helps you save in the long run.

- Stock Up During Sales: Take advantage of sales and discounts to stock up on essentials. Just be mindful of expiration dates and storage capacity.

- Prioritize Sales and Discounts:

- Shop Off-Season: Purchase seasonal items, such as clothing, decorations, or sporting goods, during off-season sales. For instance, buy winter clothing at the end of winter when stores are clearing out inventory.

- Use Cashback and Reward Programs: Enroll in cashback and reward programs offered by credit cards and retailers. These programs can provide discounts, cashback, or points on purchases, ultimately leading to savings.

- Price Comparison:

- Research Before Buying: Use price comparison websites and apps to find the best deals on products. This ensures you are getting the best price available.

- Negotiate Prices: Don’t hesitate to negotiate prices, especially for big-ticket items. Many retailers are willing to offer discounts to secure the sale.

5. Investing Wisely for Your FIRE Journey

Investing is a critical component of the Financial Independence, Retire Early (FIRE) movement. By wisely deploying your savings into various investment vehicles, you can leverage the power of compound growth to achieve financial independence more quickly. Here’s a comprehensive guide to investing wisely to support your FIRE objectives:

Diversified Portfolio

A diversified portfolio is a popular strategy for building a resilient investment plan. Diversification helps mitigate risk by spreading investments across various asset classes, sectors, and regions. Here are some common options:

- Stocks:

- Domestic Stocks: Include a variety of large, mid, and small-cap stocks from different sectors within your home country to balance growth and risk.

- International Stocks: Invest in companies outside your home country to gain exposure to global markets and diversify geographic risk.

- Bonds:

- Government Bonds: These are generally low-risk and offer stability to your portfolio. U.S. Treasury bonds, for instance, are considered one of the safest investments.

- Corporate Bonds: These can offer higher yields compared to government bonds but come with higher risks. Include a mix of investment-grade and high-yield bonds to balance safety and return.

- Real Estate:

- Rental Properties: Purchase residential or commercial rental properties. Rental income can provide substantial monthly cash flow, and property value may appreciate over time.

- Real Estate Investment Trusts (REITs): If direct property ownership isn’t for you, consider investing in REITs. These are companies that own, operate, or finance real estate and pay dividends to investors.

- Commodities:

- Precious Metals: Precious metals like gold can provide a hedge against inflation. However, it’s important to note that gold prices could be highly volatile. According to research from the World Gold Council, while gold may barely outpace inflation in the long term, it does not appreciate significantly.

- Agricultural Commodities: Including commodities like wheat, corn, or coffee can further diversify your investment portfolio.

- Alternative Investments:

- Cryptocurrencies: For those willing to take on more risk, cryptocurrencies like Bitcoin or Ethereum can offer high reward potential.

- Peer-to-Peer Lending: A relatively new and untested method of borrowing and lending money. Peer2Peer investing is where you lend a fellow American money through an online platform and are paid back in interest. The platform would help vet the borrower’s credit score and to split your investment across a number of borrowers to reduce the danger of default.

Diversified appropriately can reduce the impact of poor performance in any single area.

Low-Cost Index Funds

Low-cost index funds are a popular choice among FIRE enthusiasts due to their broad market exposure and minimal fees. They offer a straightforward, cost-effective way to achieve long-term growth. Here’s why and how to invest in them:

- Broad Market Exposure:

- S&P 500 Index Funds: These funds invest in the 500 largest publicly traded companies in the U.S., offering exposure to a wide range of industries.

- Total Market Index Funds: These funds invest in thousands of companies across the entire U.S. stock market, providing even broader diversification.

- Total International Stock Index Funds: These funds provide exposure to non-U.S. developed and emerging markets.

Learn more about index funds on A Step-by-Step Baby’s Guide to Financial Independence and Early Retirement

- Low Fees:

- Expense Ratios: Index funds typically have much lower expense ratios compared to actively managed funds, meaning more of your money stays invested and working for you.

- Minimize Fees: Over time, even small differences in fees can add up to significant amounts. Choosing low-cost funds is crucial for maximizing returns.

- Long-Term Growth:

- Historical Performance: Index funds, while not immune to market downturns, have historically provided solid returns over the long run. For example, the S&P 500 index fund has provided an average annual return of around 10% since its inception in 1957. Despite experiencing market downturns like the 2008 financial crisis, it has consistently rebounded and delivered strong returns over the long run.

- Passive Investment: They require relatively little maintenance, making them an ideal choice for a “set it and forget it” approach to investing.

Using a combination of domestic and international index funds can provide comprehensive market exposure and diversification.

Conclusion

Achieving FIRE for a family with a single income is undoubtedly challenging, but it is attainable with a thorough understanding of financial principles and disciplined execution. By creating a robust financial plan, maximizing income, minimizing expenses, investing wisely, and involving the entire family, you can work towards financial independence and the possibility of an early retirement. Embrace the journey as a family adventure, and remember that the long-term rewards—freedom, security, and peace of mind—are well worth the effort.

2 Responses

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Sure thing, could you share your specific questions so I can address them more effectively?