Photo by Towfiqu barbhuiya on Unsplash

Retirement is one of the most complicated and important matters of personal finance that the average person must contend with. Not only does it demand long-term discipline in savings, those who want to retire also have to account for inflation, tax-shelters, social security, annuities, and a host of other things besides.

As such, it’s no wonder then that the 4% rule is so popular. No need to think about these difficult details, one only needs to calculate their annual expenses, multiply that by 25 (the reciprocal of 0.04 or 4%), and they’ll have the total amount they need to fund 30 years of retirement.

Example: Jim has $40k in annual expenses. To retire in his 60’s, he’ll need $1,000,000 ($40k X 25).

Many finance experts are suspicious of the simplicity of the 4% rule. Certainly it makes retirement planning much easier (just save until you hit your number!) but is it perhaps too simple? And lest we forget, the 4% rule was first established 30 years ago, does this rule still apply today in a post-pandemic economy?

Origins of the 4% Rule

The 4% rule was first proposed by one William Bengen in his seminal 1994 study Determining Withdrawal Using Historical Data. Financial advisors of the time applied average returns and average inflation rates when making their recommendations. Since the stock market returned an average of 10% annually with an average inflation of 3%, surely this meant retirees can safely withdraw 6% from their portfolios every year, given a 50/50 stock-bond split?

Bengen wasn’t so sure. Rather than using averages, he backtested different withdrawal rates according to various periods of the US stock market history. Bengen wanted to know – if you retired at the worst possible time in history with both the worst returns and worst inflation rates, how much can you safely withdraw every year?

As it turns out: 4%.

Assuming somewhere between a 75/25 and 50/50 stock-bond split and 30 years spent in retirement, you’re safe to withdraw 4% on the first year of retirement and up your withdrawals by inflation in every subsequent year.

Criticism of Bengen’s Study

Since the paper’s release, many criticisms have been levied against the 4% rule and Bengen’s methodology. These complaints can largely be summed up as.

Too conservative

- Far too Pessimistic – The 4% rule is intended to account for the worst case scenario of the stock market’s history in combination with terrible inflation rates. The odds of retiring precisely at the worst time is, historically speaking, really really low. Going into your retirement expecting the absolute worst will lead to you leaving potentially over a million dollars of your hard-earned savings on the table.

- Lots of Leftover Money – In Bengen’s study, 96% of people pass away with the same amount of money in their portfolio as when they first retired. This means the vast majority of retirees could have spent far more money in their retirement than they actually did. With a more flexible spending plan and effective guardrails in place, retirees would be much better positioned to make the most of their golden years without putting their retirement in jeopardy.

- No Other Income Stream – Although social security alone is not enough to fund your retirement, it’s still a significant boost to your monthly income that you need to account for. That’s not even to mention pensions, annuity contracts, and potential rental income from real estate.

Want to learn more about building multiple streams of income? Check out our articles, Side Hustles to Accelerate Your FIRE Journey and How to Retire Early on a Low Income.

Too generous

- The US Stock Market Performance is Unsustainable – There’s an argument to be made that the US stock market performance is the result of luck and survivorship bias. Several historical events, from the Cuban Missile Crisis to WWII, would have capsized the US market but did not by dint of good fortune. In a 2022 paper, university finance professors write that a broad sample of developed economies like the UK, EU, Japan alongside the US make for a much better metric than just the US market. With their reassessment, the paper argues that the safe withdrawal rate should be revised to 3.02%-2.5%.

- Historical Sample Size is too Small – Bengen back tested every era of US stock market history, but as it’s not a very long history, this really only means 4 separate time periods of retirement with a lot of overlap. Under this new light, we can see how the 4% rule may not be as universal as we thought.

- Lower Bond Yields – Today the 10 year US Treasury bond yield sits at a modest 3.96%, as opposed to the 5.2% of Bengan’s day. According to the Financial Samurai, that lowers the safe withdrawal rate to about 3%.

- Longer Life Expectancy – The global life expectancy has been on an upward trend since the industrial revolution. For the purposes of retirement planning, this can mean an entire unforeseen decade you may need to account for. This is especially prescient to those of us who seek to retire early, whether that be 50’s or even younger. The 30 guaranteed years of the 4% rule no longer look to be enough.

Before closing out this section, it should be noted that Bengen himself recently came out against the 4% rule. The now-retired financial planner reassessed his calculations and came to the conclusion that the 4% rule is too conservative and in fact should be revised upward to 4.7%.

Alternatives to the 4% Rule

There are elements from both schools of thought that are useful to those of us pursuing FIRE.

The 3% Rule

Among Bengen’s various detractors, the 3% rule is a much favored alternative. Rather than withdraw 4% of your nest egg every year, you withdraw 3%. Given this adjustment, you’ll need to save 33X your annual expense rather than 25X.

Nest egg you need for $40k retirement income at 4% rule –> $1,000,000

Nest egg you need for $40k retirement income at 3% rule –> $1,320,000

As Bengen’s own study found, the 3% rule lasts at least 20 years longer than what the 4% rule promised. It will likely last even longer, if his musings are anything to go by.

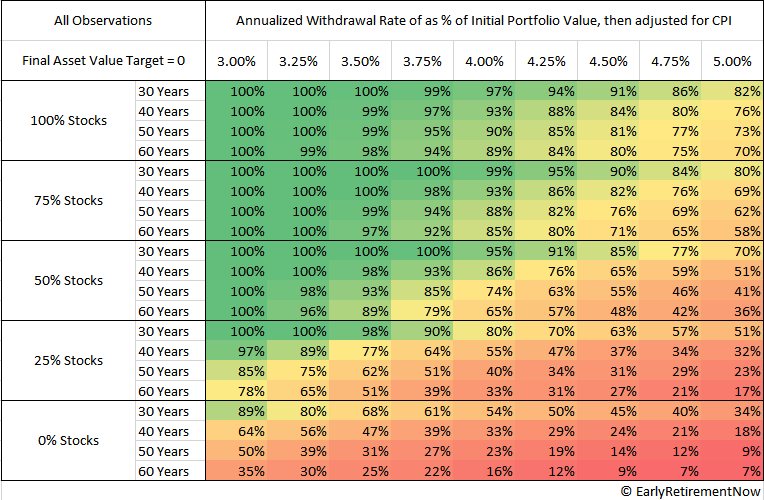

We can also compare Bengen’s conclusions with those of Early Retirement Now, in a blog article published in 2016. This study compares different stock/bond splits in portfolio allocation:

Source: Early Retirement Now

So that’s it? Instead of withdrawing 4% of your investment every year, you withdraw 3% and all your problems are solved? Well, not quite.

Adopting the 3% rule alone doesn’t address the matter of market fluctuation and the unexpected expenses of life. 50 years may be a lot longer than 30, but is it really enough for someone who aspires to retire in their 40’s or even 30’s? Not to mention, retiring when you’re still young and active means a lot more potential fluctuation in spending, for example downpayment on a new house, or a big ski trip to the Swiss Alps. If you want to make the most of your retirement savings, you’ll want to combine the 3% rule with…

Flexible Spending – The Guardrail Method

Flexible spending is exactly what it sounds like. When the stock market is performing well, you can up your withdrawals to 5% or even 6% and take that big trip. When the stock market is struggling, you can cut back on your spending and withdraw only 2% for the year to make up the difference with your cash fund.

In addition to being flexible with your expenses, you can incorporate guardrails to guide your long-term spending. The idea is if your total nest egg has dramatically grown or decreased as a result of market movements, you would recalculate your annual withdrawal amount.

For example, if you had a total nest egg of $1 million invested in the S&P 500 and you retired at 50 in 1990, using real world numbers your retirement would look something like…

4% Rule (without guardrails)

| Year of Retirement | Stock Market Returns | Inflation rate | Total Nest Egg after withdrawal | Total Nest Egg at end of year | Annual Withdrawal Amount (real inflation-adjusted) |

| 1990 | -3.06% | 6.10% | $960,000 | $930,624 | $40,000 |

| 1991 | 30.23% | 3.10% | $889,384 | $1,158,244 | $41,240 |

| 1992 | 7.49% | 2.90% | $1,115,809 | $1,199,383 | $42,435 |

| 1993 | 9.97% | 2.70% | $1,155,803 | $1,271,036 | $43,580 |

| 1994 | 1.33% | 2.70% | $1,226,270 | $1,242,579 | $44,756 |

| 1995 | 37.20% | 2.50% | $1,196,705 | $1,641,879 | $45,874 |

| 1996 | 22.68% | 3.30% | $1,594,492 | $1,956,122 | $47,387 |

| 1997 | 33.10% | 1.70% | $1,907,930 | $2,539,454 | $48,192 |

| 1998 | 28.34% | 1.60% | $2,490,491 | $3,196,296 | $48,963 |

| 1999 | 20.89% | 2.70% | $3,146,011 | $3,803,212 | $50,285 |

| 2000 | -9.03% | 3.40% | $3,751,218 | $3,412,483 | $51,994 |

| 2001 | -11.85% | 1.60% | $3,359,658 | $2,961,538 | $52,825 |

| 2002 | -21.97% | 2.40% | $2,907,446 | $2,268,680 | $54,092 |

| 2003 | 28.36% | 1.90% | $2,213,561 | $2,841,326 | $55,119 |

| 2004 | 10.74% | 3.30% | $2,784,389 | $3,083,432 | $56,937 |

| 2005 | 4.83% | 3.40% | $3,024,560 | $3,170,646 | $58,872 |

| 2006 | 15.61% | 2.50% | $3,110,303 | $3,595,821 | $60,343 |

| 2007 | 5.48% | 4.10% | $3,533,004 | $3,726,612 | $62,817 |

| 2008 | -36.55% | 0.10% | $3,663,733 | $2,324,638 | $62,879 |

| 2009 | 25.94% | 2.70% | $2,260,062 | $2,846,322 | $64,576 |

| 2010 | 14.82% | 1.50% | $2,780,778 | $3,192,889 | $65,544 |

| 2011 | 2.10% | 3.00% | $3,125,379 | $3,191,011 | $67,510 |

| 2012 | 15.89% | 1.70% | $3,122,354 | $3,618,496 | $68,657 |

| 2013 | 32.15% | 1.50% | $3,548,810 | $4,689,752 | $69,686 |

| 2014 | 13.52% | 0.80% | $4,619,509 | $5,244,066 | $70,243 |

| 2015 | 1.38% | 0.70% | $5,173,332 | $5,244,723 | $70,734 |

| 2016 | 11.77% | 2.10% | $5,172,504 | $5,781,307 | $72,219 |

| 2017 | 21.61% | 2.10% | $5,707,572 | $6,940,978 | $73,735 |

| 2018 | -4.23% | 1.90% | $6,865,843 | $6,575,417 | $75,135 |

| 2019 | 31.21% | 2.30% | $6,498,554 | $8,526,752 | $76,863 |

| 2020 | 18.02% | 1.40% | $8,448,808 | $9,971,283 | $77,944 |

| 2021 | 28.47% | 7.00% | $9,887,883 | $12,702,963 | $83,400 |

| 2022 | -18.04% | 6.50% | $12,614,142 | $10,338,550 | $88,821 |

| 2023 | 26.06% | 3.40% | $10,246,710 | $12,917,002 | $91,840 |

Pros: The 4% rule is safe for most market conditions and allows for a mostly hands-off approach to retirement. It also offers consistent withdrawal amounts for more effective long-term planning.

Cons: The 4% rule is very rigid, it’s likely to leave traditional retirees with a lot of money they never get to spend, and early retirees more vulnerable to long term bear markets.

4% Rule (with guardrails)

Rather than beginning with 4% and adjusting for inflation every year, we will set different withdrawal rates according to our total nest egg.

<$950k: 3% withdrawals

$950k-1.5M: 4% withdrawals

$1.5M-2M: 5% withdrawals

$2M-3M: 6% withdrawals

$3M-4M: 7% withdrawals

$5M-6M: 8% withdrawals

This is an approximation for what someone might do to make their spending more flexible. In a real retirement, this model would better serve as a guideline than it would as a strict rule.

| Year of Retirement | Stock Market Returns | Inflation rate | Total Nest Egg after withdrawal | Total Nest Egg at end of year | Annual Withdrawal Amount (real inflation-adjusted) |

| 1990 | -3.06% | 6.10% | $960,0000 | $930,624 | $40,000 |

| 1991 | 30.23% | 3.10% | $902,706 | $1,175,594 | $27,918 (3%) |

| 1992 | 7.49% | 2.90% | $1,128,571 | $1,213,100 | $47,023 (4%) |

| 1993 | 9.97% | 2.70% | $1,164,808 | $1,280,939 | $48,292 |

| 1994 | 1.33% | 2.70% | $1,231,344 | $1,247,720 | $49,595 |

| 1995 | 37.20% | 2.50% | $1,196,886 | $1,642,127 | $50,834 |

| 1996 | 22.68% | 3.30% | $1,542,021 | $1,891,751 | $82,106 (5%) |

| 1997 | 33.10% | 1.70% | $1,808,250 | $2,406,780 | $83,501 |

| 1998 | 28.34% | 1.60% | $2,262,374 | $2,903,530 | $144,406 (6%) |

| 1999 | 20.89% | 2.70% | $2,720,135 | $3,288,371 | $183,395 |

| 2000 | -9.03% | 3.40% | $3,098,741 | $2,818,924 | $189,630 |

| 2001 | -11.85% | 1.60% | $2,626,260 | $2,315,048 | $192,664 |

| 2002 | -21.97% | 2.40% | $2,117,761 | $1,652,488 | $82,624 (5%) |

| 2003 | 28.36% | 1.90% | $1,569,864 | $2,015,077 | $120,904 (6%) |

| 2004 | 10.74% | 3.30% | $1,894,173 | $2,097,607 | $124,893 |

| 2005 | 4.83% | 3.40% | $1,972,714 | $2,067,996 | $129,139 |

| 2006 | 15.61% | 2.50% | $1,938,857 | $2,241,512 | $132,367 |

| 2007 | 5.48% | 4.10% | $2,109,145 | $2,224,726 | $137,794 |

| 2008 | -36.55% | 0.10% | $2,086,932 | $1,324,158 | $52,966 (4%) |

| 2009 | 25.94% | 2.70% | $1,271,192 | $1,600,939 | $80,046 (5%) |

| 2010 | 14.82% | 1.50% | $1,520,893 | $1,746,289 | $81,246 |

| 2011 | 2.10% | 3.00% | $1,665,043 | $1,700,008 | $83,683 |

| 2012 | 15.89% | 1.70% | $1,616,325 | $1,873,159 | $85,105 |

| 2013 | 32.15% | 1.50% | $1,788,054 | $2,362,913 | $141,774 (6%) |

| 2014 | 13.52% | 0.80% | $2,221,139 | $2,521,436 | $142,908 |

| 2015 | 1.38% | 0.70% | $2,378,528 | $2,411,351 | $143,908 |

| 2016 | 11.77% | 2.10% | $2,267,443 | $2,534,321 | $146,930 |

| 2017 | 21.61% | 2.10% | $2,387,391 | $2,903,306 | $150,015 |

| 2018 | -4.23% | 1.90% | $2,753,291 | $2,636,826 | $152,865 |

| 2019 | 31.21% | 2.30% | $2,483,961 | $3,259,205 | $228,144 (7%) |

| 2020 | 18.02% | 1.40% | $3,031,061 | $3,577,258 | $231,338 |

| 2021 | 28.47% | 7.00% | $3,345,920 | $4,298,503 | $343,880 (8%) |

| 2022 | -18.04% | 6.50% | $3,954,623 | $3,241,209 | $226,884 (7%) |

| 2023 | 26.06% | 3.40% | $3,014,325 | $3,799,858 | $234,598 |

Pros: Guardrail Method makes better use of your investments and hedges your portfolio in case of poor stock market performance.

Cons: This method comes with a significant degree of volatility in your post-retirement income. You also need to be more hands-on in your money management to make it work.

Some Thoughts on the 4% Rule and the Guardrail Method

In a well-performing stock market (as was the case from 1990 to 2023), the 4% rule leaves the aged retiree a jaw-dropping amount of money they have no time left to spend. However, in a less than ideal market, the 4% rule may leave the same 50-year-old retiree without funds by their 80th birthday.

Will you be fulfilled after an early retirement? Read our article: How can I be happy in early retirement?

In this, we can clearly see how the Guardrail Method is superior. The example above demonstrates how a retiree can withdraw more money from their nest egg while still growing the principal, and manage a period of poor stock market return at the same time.

The main downside of the Guardrail Method is the abrupt drop in retirement income when the stock market slows. Going by the chart above, you would have been withdrawing six figures from your portfolio for half a decade before suddenly having to cut your income in half when the 2008 recession hit.

While a dramatic difference, this volatility can still be managed. Save enough to fund a full year’s expenses when times are good and be wary of lifestyle inflation. With proper planning and foresight, bear markets are nothing to fear. And remember, the stock market is not the only factor at play when you’re in retirement…

Other Factors In Retirement

One of the common criticisms levied against the 4% rule is the fact that it oversimplifies the various fees and additional incomes that arise. For the sake of simplicity, we’ve also left these considerations aside for the earlier calculations. Let’s address them now.

Tax

Just as regular income is taxed, investment income is also taxed. Getting your income taxed twice in this manner is not ideal as it eats into your compounding and makes saving for retirement and managing retirement withdrawals much more difficult than what’s shown above.

To mitigate this, many people turn to retirement tax shelters. There are many different types of tax shelters but for now we will look at the four most common ones.

| 401(k) | Roth 401(k) | Traditional IRA | Roth IRA |

| Offered by company – Employer match a percent of your contributions – Investment options depends on company | Offered by company – Employer match a percent of your contributions – Investment options depends on company | Self-directed – Open to most financial investments | Self-directed – Open to most financial investments |

| Higher contribution limits – 23k in 2024, employer match does not count towards the limit – cumulative across all 401(k)s | Higher contribution limits – 23k in 2024, employer match does not count towards the limit – cumulative across all 401(k)s | Lower contribution limits – $7k in 2024 – cumulative across all IRAs | Lower contribution limits – $7k in 2024 – cumulative across all IRAs |

| Don’t pay regular income tax – contributions are tax-deductible, then pay tax on withdrawal | Don’t pay investment income tax – contributions are not tax-deductible, withdrawals are not taxed | Don’t pay regular income tax – contributions are tax-deductible, then pay tax on withdrawal | Don’t pay investment income tax – contributions are not tax-deductible, withdrawals are not taxed |

Beware: as these tax shelters are geared towards traditional retirement, you will be penalized for making early withdrawals (before age 59 1/2). There are some exceptions to these rules, if you’re withdrawing money for medical expenses, first time home purchases, educational expenses, etc. Additionally, there are penalties for not withdrawing the Required Minimum Distribution by age 72. The RMD penalty applies to traditional 401(k) and IRA, but not Roth IRA. After 2024, it will also no longer apply to Roth 401(k).

To learn more about this topic, check out our articles on How to Withdraw Money from Roth IRA Without Penalty, How to Take Money Out of 401(k) Early Without Penalty, How to Retire Early with No Penalty, Best Withdrawal Strategies for Early Retirement, and Tax Strategies on FIRE.

Investment Fees

There’s a wealth of different stock investment options, from mutual funds where many investors pool together their resources for a single professional to manage, to ETFs that more specifically targets a sector for investing. You can even get adventurous and pick your own stocks.

In terms of keeping investment costs down, monthly contributions to a broad-based index fund is the way to go. Mutual funds charge significant management fees while stock picking means paying transaction fees for every purchase and sale. Something like the S&P 500 is comparatively cost-effective, with rock-bottom management fees and little to no transaction fees due to minimal turnover.

Bonds

Today’s bonds aren’t attractive investment options. US Treasury Bonds over 10 years is 3.91%, or barely covering inflation. It’s not competitive with high yield savings accounts, some of which offer as much as 5%. At more lucrative (and more risky) rates, the current economy offers a 13.69% yield for CCC bonds at 21% rate of default. Compared to that, the stock market would be preferable with its higher returns and lower risk of default.

The main use of bonds would not be to build wealth. In fact it’s barely able to retain wealth. What it can offer is stability, specifically for if you’ve hit your 80’s or even 90’s and now seek to keep your nest egg somewhere safe and stable.

Social Security

Social security is calculated according to how much money you made in your working career, when you decide to begin taking out your social security, and what the general economy looks like at the time of your retirement.

Social security alone is not enough to fund a retirement, but it’s not an insignificant contribution to your own savings. Social security additions can help smooth out the Guardrail Method and factoring it in can let you retire with a smaller retirement fund than previously thought. As a rule of thumb, the sooner you start taking out social security, the higher your safe withdraw ceiling, the later you start taking out social security, the higher your safe withdraw floor.

It’s a good idea to get an estimate of the amount you’ll get in social security so you can better plan your retirement.

Annuities

This is a type of financial product where you pay a company a large sum of money in exchange for future fixed monthly payments. Exactly how much you get for the amount you pay is dependent on an entire web of factors. How old are you currently? Do you want fixed payments for life or just a certain number of years? Do you want to leave guaranteed inheritance? What’s your gender? What’s your medical history?

Ideally you’ll want to shop around and see what your options are. Annuities can be monstrously complicated so we recommend not buying one unless you know the ins and outs of your contract.

For a ballpark of how much you’ll get as a man – for a $500k annuity, we’re looking at $3,049/month at 60, $3,303/month at 65, $3,652/month at 70, and capping out at $4,080/month at 75.

Depending on your unique situation, an annuity might be a more preferable retirement tool than bonds.

Real Estate

Practically speaking, the best thing about owning a home is the safety and security of having a comfortable low-cost place to live in your golden years. Real estate can also make for great income streams, if you happen to have multiple properties that you can rent out.

Life Expectancy

Along with rising life expectancy comes rising health care costs. Going by our earlier charts, it may be tempting to reduce your retirement savings goal to $700k or even $500k. It’s important to remember that not only are extended bear markets still very possible, your health care costs can go up dramatically at the tail end of your life.

It’s better to assume that you’ll live longer than you do rather than the other way around.

Conclusion

As we hope this article has made abundantly clear, the 4% rule is a hilariously simple guideline for an incredibly complex matter. However, this doesn’t mean the 4% rule isn’t helpful. Having an easy clear guideline for what is generally safe can be invaluable for retirement planning.

Is the 4% rule obsolete?

For our money, no. But on its own the 4% rule is not enough to capture the full picture of retirement. We have gone over many details and facets of retirement in this fairly long article and still have not covered them all. What of pensions? What of sharing retirement with a spouse?

Even so, we hope that just like the 4% rule, our simplified overview of what retirement might look like is helpful to you. What matters is not following the rules and guidelines to the letter, but leveraging them to best suit your own circumstance and your own life. When you start working toward a meaningful goal, the result is always far better than setting off with no goal at all.

Best of luck to you and your retirement!

Did you find this article helpful? Check out our other articles for more tips to accelerate your journey to Financial Independence!

How to Retire Early with No Money

Master FIRE Money Management: Your Blueprint for Early Retirement

2 Responses

thanks for info.

이 기사는 절대적으로 정확합니다. 이 훌륭한 웹사이트는 훨씬 더 많은 고려가 필요하다고 말해야겠습니다. 아마 다시 와서 더 많이 배울 것입니다. 이 정보에 대해 정말 감사합니다.