In recent years, the concept of Financial Independence, Retire Early (FIRE) has gained significant popularity. Among the various offshoots of this movement, LeanFIRE has emerged as a standout strategy for those seeking to achieve financial independence through a more minimalist and frugal lifestyle. Here’s what you need to know about the LeanFIRE strategy and how it can pave the way to a financially independent future.

What is LeanFIRE?

LeanFIRE is a subcategory of the broader FIRE movement that emphasizes achieving financial independence by maintaining a significantly lower cost of living. While the traditional FIRE approach often involves amassing a substantial retirement nest egg to support a comfortable lifestyle, LeanFIRE focuses on living a simplified, minimalist lifestyle with strictly controlled expenses. This allows individuals to reach financial independence relatively quickly, as they require a smaller retirement fund to cover their modest living costs.

Key Components of LeanFIRE

- Frugality: At the core of LeanFIRE is a commitment to frugality. Frugality involves a disciplined approach to spending, with a keen eye on eliminating waste and unnecessary expenses while still enjoying a fulfilling life. It’s about adopting a mindset that values sustainability and efficiency over consumerism and extravagance.

- Minimalism: LeanFIRE enthusiasts often embrace minimalism, reducing physical possessions and focusing on experiences rather than material goods. This not only helps in reducing expenses but also simplifies life, reducing stress and increasing overall satisfaction.

- Budgeting and Tracking: A crucial aspect of LeanFIRE is meticulous budgeting and tracking of expenses. This helps in identifying areas where costs can be trimmed and ensures that spending aligns with financial goals.

- Increasing Savings Rate: The cornerstone of LeanFIRE is a high savings rate. By significantly lowering living expenses, individuals can save a larger portion of their income, accelerating the path to financial independence.

- Invest Wisely: Optimizing your investments is fundamental to achieving FIRE. It’s about putting your hard-earned savings to work, generating passive income that eventually replaces your need for a traditional paycheck.

Now, let’s dive deep into the details.

1.Frugality: The Pillar of LeanFIRE

At the heart of the LeanFIRE strategy lies a powerful and transformative concept: frugality. This principle is not merely about pinching pennies or living in deprivation. Instead, frugality within the LeanFIRE framework means making deliberate, conscious choices to curb spending and prioritize saving. It’s about redefining value, focusing on what truly matters, and making financial decisions that align with long-term goals. Here’s an expanded look into how frugality forms the core of LeanFIRE and practical steps to integrate it into your daily life.

A.Understanding Frugality in LeanFIRE

Frugality involves a disciplined approach to spending, with a keen eye on eliminating waste and unnecessary expenses while still enjoying a fulfilling life. It’s about adopting a mindset that values sustainability and efficiency over consumerism and extravagance.

Embracing frugality means making conscious spending choices and seeking out the most cost-effective alternatives without compromising quality of life.

B.Deliberate Choices

The foundation of frugality is making deliberate and informed choices about where your money goes. This includes critically analyzing your spending habits and differentiating between needs and wants. By doing so, you can cut out non-essential expenses and focus on what truly adds value to your life.

- Needs vs. Wants: Start by distinguishing between your essential needs (housing, food, healthcare) and discretionary wants (luxury items, dining out). This clarity helps in directing funds toward necessary expenses while reducing frivolous spending.

- Value-Based Spending: Adjust your spending habits to align with your core values. Prioritize purchases and activities that enhance your well-being and happiness, and trim costs in areas that don’t contribute significantly to your life satisfaction.

C.Practical Steps to Cut Non-Essential Expenses

Achieving frugality requires identifying and eliminating expenses that are not essential. Here are practical steps to streamline your spending:

- Create a Budget: Establish a detailed budget that outlines your income, essential expenses, and savings goals. Track your spending to ensure it aligns with your budget and identify areas for improvement.

- Downsize Lifestyle: Consider downsizing your living arrangements. A smaller home or shared accommodation can significantly reduce housing costs. Similarly, reducing consumption of utilities by adopting energy-saving measures can lower monthly bills.

- Meal Planning and Home Cooking: Dining out can quickly deplete your budget. Instead, plan your meals, create a grocery list, and cook at home. This not only saves money but also allows you to eat healthier.

- Limit Subscriptions and Memberships: Cancel unused subscriptions and memberships. Whether it’s a streaming service, gym membership, or magazine subscription, assess whether you’re getting value from each recurring expense.

- Buy Secondhand: Embrace the practice of buying secondhand goods. Thrift stores, garage sales, and online marketplaces offer quality items at a fraction of the cost of new products.

Watch more on

D.Seeking Out Cost-Effective Alternatives

Frugality also involves actively seeking out cost-effective alternatives to everyday expenses. This means being resourceful and inventive in finding cheaper ways to meet your needs.

- DIY Solutions: Whenever possible, opt for do-it-yourself solutions. From home repairs to personal care products, learning to do things yourself can save a significant amount of money.

- Public Transportation and Biking: Reduce commuting costs by using public transportation, biking, or carpooling. This not only lowers expenses but also has environmental benefits.

- Entertainment and Leisure: Look for free or low-cost entertainment options. Community events, public parks, hiking trails, and library resources can offer enjoyable activities without breaking the bank.

- Frugal Travel: When traveling, opt for budget accommodations, use travel reward points, and seek out affordable destinations. Plan trips during off-peak seasons to get better deals.

E.Maximizing Value in Every Aspect of Life

Maximizing value extends beyond just finding cheaper alternatives. It involves making smart choices that enhance overall well-being and financial health in the long run.

- Quality Over Quantity: Sometimes spending a bit more upfront on high-quality items can save money in the long run due to durability and reduced replacement frequency. This applies to clothing, appliances, and even vehicles.

- Invest in Skills: Invest in acquiring new skills that can save money or generate additional income. Learning to cook, garden, or do basic home repairs are valuable skills that contribute to financial independence.

- Health and Wellness: Prioritize health and wellness to avoid medical expenses. Regular exercise, a balanced diet, and preventive care can lead to long-term savings by reducing healthcare costs.

- Financial Literacy: Educate yourself on personal finance. Understanding investments, taxes, and financial planning can help you make informed decisions that maximize your money’s potential.

F.Long-Term Benefits of Frugality

Integrating frugality into your lifestyle as part of the LeanFIRE strategy can yield significant long-term benefits:

- Accelerated Financial Independence: By reducing expenses and prioritizing saving, you can amass a substantial nest egg more quickly, paving the way for early retirement.

- Financial Security: Frugality fosters financial security by building a robust emergency fund and reducing reliance on debt.

- Environmental Impact: A frugal lifestyle often translates to a reduced environmental footprint, as it promotes sustainability and mindful consumption.

- Life Satisfaction: Embracing frugality can lead to greater life satisfaction by shifting the focus from material possessions to meaningful experiences and relationships.

2.Minimalism: A Core Principle for LeanFIRE Enthusiasts

Minimalism is similar to frugality and emerges as a vital principle of LeanFIRE. By embracing minimalism, LeanFIRE enthusiasts significantly reduce physical possessions and redirect their focus toward enriching experiences rather than accumulating material goods. This fundamental shift not only drives down expenses but also simplifies life, alleviates stress, and enhances overall satisfaction. Here’s an in-depth exploration of how minimalism integrates with LeanFIRE and practical ways to adopt a minimalist lifestyle.

A.The Philosophy of Minimalism

Minimalism is more than just decluttering or living with fewer things; it’s a lifestyle choice that emphasizes intentional living. It encourages individuals to question what adds value to their lives and to eliminate excess that doesn’t. By focusing on what truly matters, minimalism frees up time, space, and resources, creating a more fulfilling life centered on purpose and meaning.

B.Key Principles of Minimalism in LeanFIRE

- Intentional Living: Minimalism involves making deliberate choices about what you own and how you spend your time. It’s about curating a life filled with items and activities that bring joy and value.

- Reducing Possessions: By minimizing physical possessions, individuals can reduce maintenance costs, storage needs, and the mental burden associated with clutter.

- Experiences Over Things: Shifting the focus from material goods to meaningful experiences fosters deeper connections and lasting satisfaction.

- Simplicity and Clarity: A minimalist lifestyle promotes simplicity and clarity, leading to reduced stress and a greater sense of control over one’s environment and finances.

C.Practical Steps to Embrace Minimalism

- Declutter Your Space: Begin by decluttering your home. Assess each item for its usefulness and joy it brings. Keep only what you need and love, and let go of the rest. Donate, sell, or recycle unneeded items.

- Adopt a Capsule Wardrobe: Simplify your wardrobe by embracing a capsule collection consisting of versatile, high-quality pieces. This reduces decision fatigue and lowers clothing expenses. Watch more on

- Digitize When Possible: Convert physical documents, books, and media to digital formats. This not only saves space but also makes it easier to organize and access your belongings.

- Limit Impulse Purchases: Implement a waiting period before making new purchases. This helps in evaluating whether the item is truly necessary and aligns with your minimalist values.

- Mindful Consumption: Adopt mindful consumption practices by choosing products that are durable, multipurpose, and have a minimal environmental impact.

- Quality Over Quantity: Invest in fewer, high-quality items that last longer and fulfill your needs better than an abundance of lower-quality goods.

D.Focusing on Experiences

- Prioritize Experiences: Allocate your time and resources to experiences that bring joy and enrich your life, such as travel, hobbies, and spending time with loved ones.

- Practice Gratitude: Regularly practice gratitude for the experiences and relationships in your life. This mindset shift can increase emotional well-being and reduce the desire for material possessions.

- Community and Connection: Engage in community activities and build strong social connections. Sharing moments with others often brings more fulfillment than acquiring new things.

E. Simplifying Life

- Streamline Daily Routines: Create streamlined daily routines that eliminate unnecessary tasks and focus on productivity and well-being.

- Digital Minimalism: Reduce digital clutter by organizing files, unsubscribing from unneeded services, and limiting social media use. This helps in managing time and mental space more effectively.

- Financial Simplicity: Simplify your financial life by consolidating accounts, automating savings and bill payments, and sticking to a straightforward investment strategy.

F. Benefits of Minimalism in LeanFIRE

- Reduced Expenses: By curbing the urge to buy unnecessary items, minimalism directly contributes to lower living costs, which is essential for LeanFIRE.

- Less Stress: A decluttered, organized environment leads to reduced stress and increased mental clarity, promoting a more peaceful life.

- Greater Flexibility: With fewer possessions to manage and less financial burden, minimalists enjoy greater flexibility to pursue opportunities, travel, or adapt to changes.

- Increased Satisfaction: Focusing on meaningful experiences and relationships over material goods leads to higher overall life satisfaction and happiness.

3.Budgeting and Tracking: Essential Tools for LeanFIRE Success

The journey to achieving LeanFIRE (Financial Independence, Retire Early with a lean budget) hinges on a thorough understanding and control of one’s financial landscape. At the heart of this approach is meticulous budgeting and tracking of expenses. These practices help identify areas where costs can be trimmed, ensure that spending aligns with financial goals, and ultimately enable a more efficient path to financial independence. Here’s an in-depth look at the importance of budgeting and tracking in LeanFIRE and how to implement them effectively.

A.The Importance of Budgeting in LeanFIRE

Budgeting is the process of creating a plan to manage your money, detailing how much you earn, spend, and save over a given period. For LeanFIRE enthusiasts, a solid budget is the backbone of financial planning. It offers structure and clarity, allowing you to make informed decisions and avoid unnecessary expenses.

- Financial Awareness: Budgeting fosters awareness of your financial status, helping you understand where your money goes and how it can be managed more effectively.

- Goal Setting: It allows you to set clear, measurable financial goals, such as saving a specific amount each month or paying off debt within a certain timeframe.

- Expense Management: A budget helps in managing expenses by delineating between essential and non-essential costs, making it easier to prioritize and make cuts where necessary.

- Savings Maximization: By controlling expenses and avoiding overspending, budgeting ensures that a larger portion of your income can be directed toward savings and investments.

B.Key Steps to Create an Effective Budget

- Assess Your Current Financial Situation: Start by gathering all your financial information, including income, expenses, debts, and assets. This assessment provides a baseline for your budget.

- Categorize Expenses: Divide your expenses into categories such as housing, utilities, groceries, transportation, entertainment, and so on. This helps in identifying spending patterns and areas for potential savings.

- Set Financial Goals: Define your short-term and long-term financial goals. This could include building an emergency fund, saving for retirement, or paying off loans. Your budget should reflect these priorities.

- Allocate Income: Allocate portions of your income to each expense category based on your needs and goals. Ensure that essential expenses are covered first, and allocate the remaining income towards Savings and discretionary spending.

- Create a Buffer: Include a buffer in your budget for unexpected expenses. This helps in managing unforeseen costs without disrupting your financial plan.

Read more on FIRE Budgeting 101: Your Essential Guide to Financial Independence

C.Practical Tools for Budgeting and Tracking

- Budgeting Apps: Utilize budgeting apps like WeFIRE which offers easy-to-use interfaces for setting budgets, tracking expenses, and receiving alerts.

- Spreadsheets: Create a budget spreadsheet using software like Microsoft Excel or Google Sheets. This customizable option allows for detailed tracking and analysis of your finances.

- Envelope System: A traditional approach where you allocate cash into envelopes for different spending categories. Once an envelope is empty, you can’t spend more in that category until the next budget period.

- Financial Journals: Maintain a financial journal where you manually record each transaction and review it regularly. This can be particularly effective for those who prefer a hands-on approach.

D.Tips for Effective Budgeting and Tracking

- Use Categories Wisely: Keep expense categories simple and broad enough to avoid becoming overwhelmed but detailed enough to provide insight into spending habits. Too many categories can make tracking tedious.

- Automate Savings: Automate your savings by setting up automatic transfers from your checking account to your savings or investment accounts. This ensures that savings are prioritized.

- Consistency: Be consistent with tracking your expenses. Set aside time daily or weekly to update your records and review your budget.

- Review Regularly: Regularly review your budget and expenses to ensure they align with your financial goals. Adjust your budget as necessary to address changing circumstances or goals.

- Be Realistic: Set realistic spending limits and goals based on your actual income and expenses. An overly restrictive budget can be difficult to maintain and lead to burnout.

- Stay Flexible: Life is unpredictable, and so are finances. Stay flexible and be willing to adjust your budget and tracking methods as needed.

4.Increasing Savings Rate: The Cornerstone of LeanFIRE

The idea is simple but powerful: by significantly lowering living expenses, individuals can save a larger portion of their income. This increased savings rate is the key to rapidly accumulating the financial resources needed for early retirement. Here’s an in-depth look at why a high savings rate is crucial to LeanFIRE and how to effectively boost your savings rate.

A.Why a High Savings Rate Matters

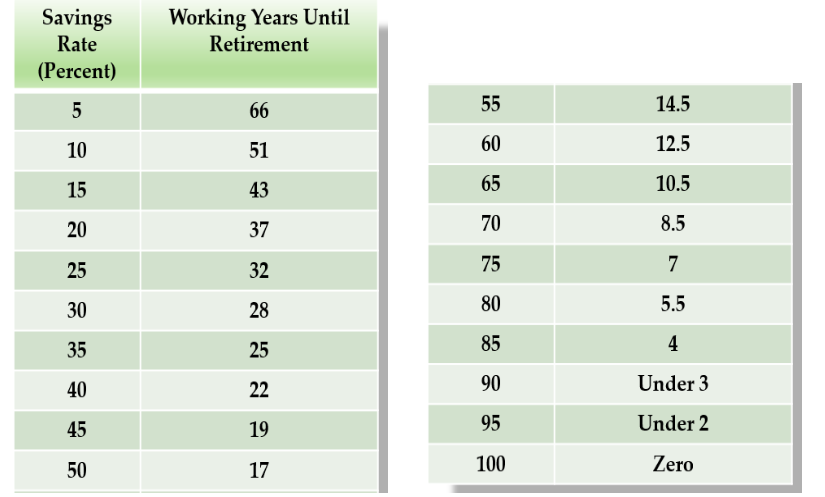

Savings rate has a direct correlation to the years to financial independence. If you save a substantial percentage of your take-home pay, such as 50%, and live on the remaining 50%, you’ll be financially independent in a reasonable number of years—about 17 years, according to networthify.com.

Screenshot from networthify

The table below from Mr. Money Mustache shows how many years you will have to work for a range of possible savings rates, starting from a net worth of zero:

The charts are based on some conservative assumptions, including:

- You can earn a 5% return on your investments after inflation during your saving years.

- You’ll live off the “4% safe withdrawal rate” after retirement, with some flexibility in your spending during recessions.

- You want your ‘Stash to last indefinitely, touching only the gains.

As you can see, the savings rate significantly impacts the time it takes to achieve financial independence. The more you save, the lower your required nest egg, reducing the amount needed to sustain your retirement. Additionally, higher savings allow your investments to grow more, exponentially increasing your wealth.

B.Strategies to Increase Your Savings Rate

- Lower Living Expenses: The most direct way to increase your savings rate is to reduce your living expenses. Evaluate your budget and identify opportunities to cut costs. Read more on Best Way to Save Money for Early Retirement

- Increase Income: Another way to bolster your savings rate is by increasing your income. Read more on Side Hustles to Accelerate Your FIRE Journey ; How to Retire Early from Real Estate Investing

- Automate Savings: Make saving effortless by setting up automatic transfers from your checking account to savings or investment accounts. Additionally, maximize contributions to employer-sponsored retirement plans like 401(k)s or 403(b)s, especially if your employer offers matching contributions. Read more on Tax strategies on FIRE

- Minimize Debt: High-interest debt can severely impact your ability to save. Focus on paying off debts to free up more of your income for savings. If you currently have debts, read more on How to Retire Early When You Have Debts

- Adopt a Frugal Lifestyle: Embrace frugality across all aspects of life.

C.The Psychological Aspect of Saving

Increasing your savings rate isn’t just about the numbers; it’s also about mindset.

- Delayed Gratification: Train yourself to resist the lure of immediate pleasures in favor of long-term benefits. This psychological shift is crucial for sustained saving.

- Financial Goals: Set clear and motivating financial goals. Whether it’s retiring by a certain age, buying a home, or traveling the world, having a goal helps maintain discipline.

- Tracking and Progress: Regularly track your saving progress and celebrate milestones. This reinforces positive behavior and keeps you motivated.

Read more on How to Stay Motivated When FlRE is Years Away?

D.Potential Challenges and Solutions

- Lifestyle Inflation: As income increases, resist the temptation to inflate your lifestyle. Maintain a modest standard of living to continue maximizing savings.

- Social Pressure: Peer pressure can lead to unnecessary spending. Surround yourself with like-minded individuals who support your financial goals and adopt a less consumerist lifestyle.

- Sustainability: Ensure that your saving methods are sustainable. Avoid extreme measures that could lead to burnout or detract from quality of life. Balance is key. Read more on Does FIRE Mean Living Frugally

5. Optimize Your Investments

Like any FIRE strategy, investments are crucial for achieving financial independence. At its core, FIRE involves accumulating wealth through disciplined savings and strategic investments so that your assets generate enough passive income to cover living expenses indefinitely. It’s essential to approach investing strategically, aligning your choices with your risk tolerance and long-term FIRE goals.

FIRE-Friendly Investment Options:

Index Funds: The Simple and Effective Path: Index funds are investment vehicles that track a specific market index, such as the S&P 500 or the Nasdaq Composite. They offer instant diversification by holding a basket of stocks or bonds that mirror the index’s composition. Index funds are favored by FIRE enthusiasts for their simplicity, low fees, and historical track record of delivering solid returns over the long term. They require minimal maintenance and are an excellent choice for beginners and seasoned investors alike. For more detailed guidance, refer to this article:A Step-by-Step Baby’s Guide to Financial Independence and Early Retirement

Stocks: The Potential for Higher Returns: Investing in individual stocks can be a rewarding endeavor, offering the potential for higher returns than index funds. However, it often comes with greater volatility. Thorough research and a solid understanding of market dynamics are essential for successful stock picking. It’s advisable to diversify your stock portfolio across different sectors and industries to mitigate risk.

Other Options: Diversifying Your Portfolio: Depending on your risk appetite and financial knowledge, you can explore other investment options like bonds, dividend-paying stocks, or even starting your own business. Diversifying appropriately helps spread risk and ensures that your portfolio isn’t overly reliant on a single asset class.

Conclusion

LeanFIRE offers a practical route to financial independence for those with modest incomes who are ready to embrace a frugal and minimalist lifestyle. By focusing on reducing expenses, saving aggressively and investing wisely, individuals can achieve financial freedom earlier and enjoy the peace of mind that comes with living within their means.

Y H